Whether choosing the option for higher pension amount under the EPS 95 scheme is good or not for you is what we will try to analyse in this blog using some calculations. Also, you will find a calculation which may be able to suggest you how long your un-transferred portfolio may last, in case you do not opt to switch your EPF contribution to EPS?

As a preparation, some other organisations have also started asking its employees on whether they would like to switch to higher pension option.

Let’s start by understanding our PF statement. For the purpose of this blog we will take Salary = Basic + DA

The contribution to your EPF amount consists of 3 parts –

- Employee contribution – 12% of Salary

- Employer contribution – 12% of Salary (divided into 2 parts)

- 8.33% of this goes to Employee Pension Scheme (EPS) against which you will be getting pension

- Rest 3.67% goes to Provident Fund.

Part-1 History of EPS 95 Scheme

1995 to Sep – 2014

Employer Share in EPF = 3,000 – (8.33% of 6,500) = 3,000 – 541 = 2,459

After Sep-2014

After FY 2021-22

Part-2 Comparison with Higher Pension Scheme option

Before Sep-2014 (Comparison)

After Sep-2014 (Comparison)

After FY 2021-22 (Comparison)

Part 3 – Reality of 8.33%

If you are wondering why this weird percentage of 8.33% has been taken to calculate EPS contribution, then lets have a look at this example.

Thus, what you are contributing really is 1/12th of your Salary on a monthly basis and if you convert 1/12 in percentage terms, it comes to be 8.33333333….% which has been rounded off to 8.33%

And this, in 1 year, assuming your salary remains constant, you contribute portion equivalent of 1 month of salary to your EPS account.

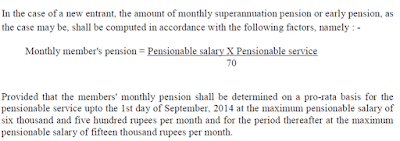

Part 4 – How is Pension Calculated?

Below is an extract from the EPS Scheme document which clearly prescribes the formula for calculating of Monthly Pension.

Let’s under this better with the help of an example –

As you can see that in 3rd option, one can get much higher pension (literally no ceiling) and that is why people went to court for it.

Part 5 – Getting Higher Pension

We have seen that going by the rules, if we want the Pension on actual salary amount, then our 8.33% contribution to EPS should also have been on the actual salary amount.

But since we have been contributing on the reduced (ceiling) pension of either 6,500 or 15,000, hence our contribution of EPS has been much lesser than what it should have been.

Let’s revisit this using the examples we have taken previously.

To get this excess salary of 42,500 (50,000 – 7,500), you need to make

EXCESS Contribution in EPS = 8,330 – 1,250 = 7,080 per month

and you will get

LESS Contribution in EPF = 10,750 – 3,670 = 7,080 per month

Simplistically, for above case, by paying 7,080 per month today you will get extra pension of 42,500 per month at retirement. BUT, it is NOT that simple else why would you be asking this question!!!

Part 6 – Problem for people

First, for people who have already retired (in 2014 or after), they will have to deposit the excess amount (including interest) with PF which will be contributed to EPS portion and for many people it will be a challenge to deposit the amount. They would have either invested that amount somewhere or may find it difficult to part with such a big sum of money.

Second, the pensionable salary is being calculated as an average of last 60 months salary (as opposed to previous case of average of 12 month salary). This may bring a lot of variation for people who had significant increase in their salaries towards the last couple of years before retirement.

Lastly, for people who joined EPF before 2014 but have not yet retired, they will have to perform cost-benefit calculation to see whether its worth parting with their previous EPF contribution. Though, as compared to the already retired people, they won’t have to take the pain of depositing the sum of money which they have previously withdrawn (except for cases who have taken loan or advances)

For people who have retired before 2014, this option is NOT available.

Part 7 – Should you Opt for higher Pension

Let’s visually revisit the example we saw in Part 5

Now, things have become interesting. So, over the 35 years period, the total difference of Principal + Interest comes to be 1,58,11,138. And so, you need to forego this amount to be able to get extra 42,500 as pension. What do you think of this now?

Observe that if you simply start withdrawing 42,500 per month from your excess corpus of 1,58,11,138 (approx. 1.6 Crore) and assume this is not getting any interest accrued on it, it will take you 373 months to exhaust the entire corpus which means approx. 31 years.

If you deposit this excess 1.6 Crore in a Bank FD at even 6% Rate of interest, you will earn a monthly interest of 80,000 (in reality it will be slightly less if you take monthly payouts). Along with that you will also have your capital preservation of 1.6 Crore which will remain with you and your heirs.

Part 8 – The TWIST

So, while it seems like taking the corpus away makes sense, but it may not make sense for most people.

0 Comments